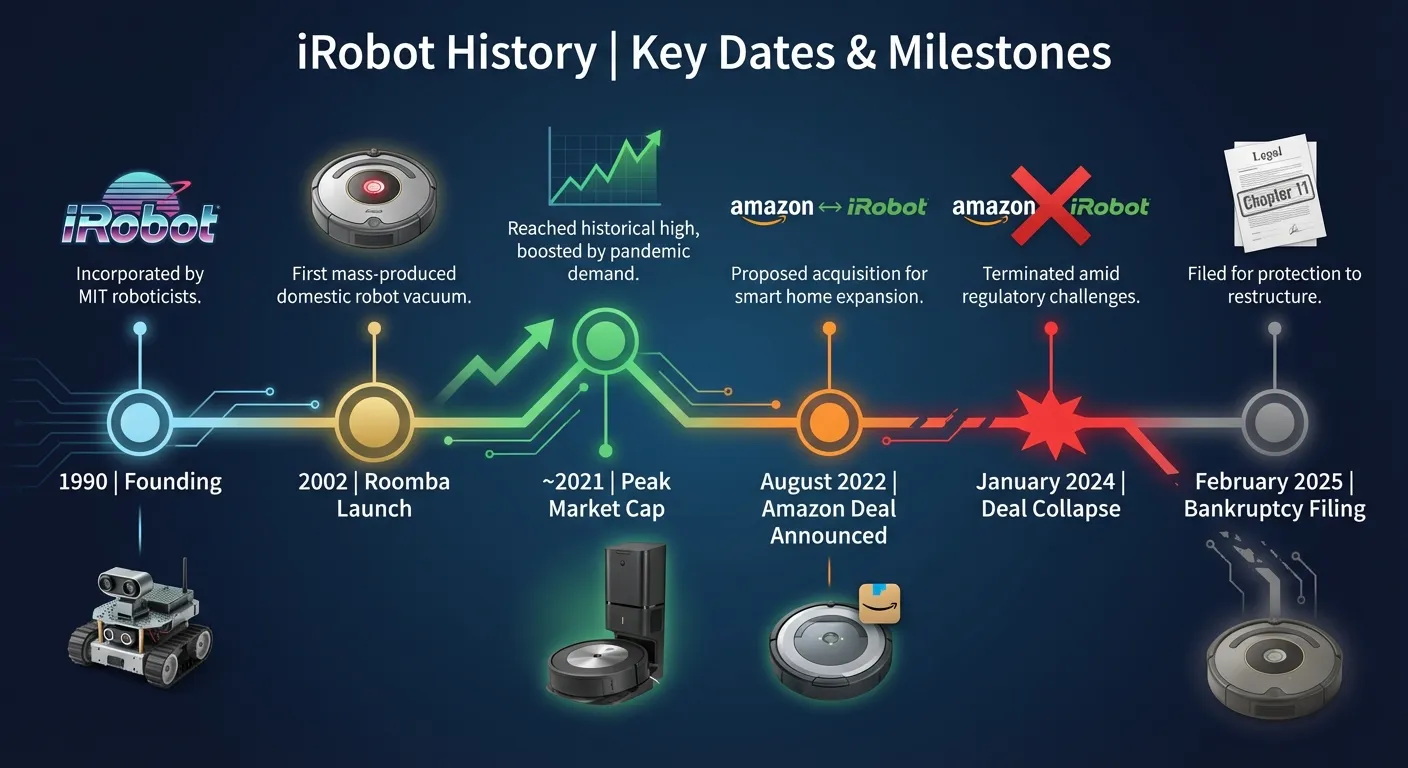

iRobot filed for Chapter 11 bankruptcy protection today, a sentence that would have seemed inconceivable a decade ago when the Bedford, Massachusetts company dominated the robotic vacuum market so thoroughly that "Roomba" had become the generic term for the entire product category. The filing lists $435 million in liabilities against $214 million in assets, a balance sheet that tells the story of a company that pioneered an industry and then watched that industry outgrow it.

The bankruptcy arrives less than two years after Amazon abandoned its planned $1.7 billion acquisition of iRobot, a deal that collapsed in January 2024 under regulatory pressure from the European Commission and the Federal Trade Commission. Colin Angle, iRobot's co-founder and CEO from its 1990 founding until his departure in May 2025, told the Wall Street Journal at the time that the acquisition's failure "removed the only realistic path to competing at the scale our market now requires." He was right. In the twenty months since, iRobot's quarterly revenue declined 42%, its stock price fell below $2, and the workforce shrank from 1,400 to approximately 300.

The Rise: From MIT Lab to Every Living Room

iRobot's origin story reads like a Silicon Valley parable, except it happened on the East Coast. Three MIT Artificial Intelligence Lab researchers, Colin Angle, Helen Greiner, and their advisor Rodney Brooks, founded the company in 1990 with a vision of building practical robots for real-world applications. Their early work focused on military reconnaissance robots, including the PackBot, which became widely used by the U.S. military for bomb disposal in Iraq and Afghanistan.

The consumer pivot came in 2002 with the first Roomba, priced at $199. Industry analysts were skeptical. Jim Estill, then a tech distributor and early investor, recalled to CNBC that "the consensus was that nobody would pay two hundred dollars for a vacuum that couldn't get into corners." The consensus was spectacularly wrong. iRobot sold over a million Roombas in the first two years, and the product became one of the most successful consumer electronics launches of the 2000s. By 2020, the company had sold over 30 million units worldwide and commanded roughly 44% of the global robot vacuum market, according to Euromonitor International.

The Fall: When Innovation Meets Manufacturing Economics

iRobot's decline is a case study in a phenomenon that business strategists call the "pioneer's penalty." The company spent heavily on R&D to create and refine the category, investing over $1.5 billion in research across its lifetime according to SEC filings. Competitors, primarily Chinese manufacturers including Ecovacs, Roborock, and Dreame, entered the market after the technology was proven, reverse-engineered the core functionality, and manufactured at dramatically lower costs.

By 2024, a competent robot vacuum from Roborock cost $300. A comparable Roomba cost $800. The Roborock featured lidar navigation, self-emptying capability, and mopping functionality. The Roomba offered iRobot's brand reputation and what the company argued was superior software intelligence. Consumers, overwhelmingly, chose the cheaper option. Ben Bajarin, CEO of the market research firm Creative Strategies, told TechCrunch that "iRobot suffered from the classic innovator's dilemma: they made a premium product in a market that commoditized faster than anyone expected."

The Amazon acquisition would have solved this problem by integrating Roomba into Amazon's ecosystem, subsidizing hardware costs through data monetization and Alexa integration. When that path closed, iRobot had neither the manufacturing scale to compete on price nor the ecosystem lock-in to justify its premium. The company cut costs aggressively, reducing its workforce multiple times and exiting product lines including lawn mowers and pool cleaners, but the revenue decline outpaced the cost reductions.

The Data Controversy That Eroded Trust

iRobot's struggles were compounded by a privacy scandal that damaged the brand's most valuable intangible asset: consumer trust. In December 2022, MIT Technology Review reported that images captured by Roomba's development-model cameras had been shared with Scale AI, a data labeling contractor whose workers posted some of those images, including images of people in private settings, to social media. iRobot maintained that the images came from special data-collection units used by paid testers who had signed consent agreements, not from consumer products.

The distinction mattered legally but not commercially. The incident landed during the Amazon acquisition review, where privacy concerns about a home-mapping robot were already central to the regulatory debate. The European Commission's objections to the Amazon deal focused on competitive concerns, but the privacy scandal gave regulators additional ammunition: the prospect of Amazon, already the dominant smart home platform, gaining access to detailed interior maps of millions of homes became harder to defend publicly after the MIT Technology Review report demonstrated how Roomba data could be mishandled. Consumer surveys conducted by Parks Associates in 2023 showed that "data collection concerns" had become the second most-cited reason, after price, for choosing a competitor over Roomba.

What Happens to Roomba Now

The Chapter 11 filing allows iRobot to continue operations while restructuring its debt and exploring strategic alternatives, which in practice means finding a buyer for the Roomba brand and its patent portfolio. Several potential acquirers have been discussed in industry media, including Samsung (which makes its own robot vacuums), SharkNinja (which has been expanding its floor care lineup), and private equity firms that specialize in distressed consumer brands.

The Roomba brand retains meaningful value despite the company's financial collapse. Consumer awareness remains high, and the installed base of over 40 million units worldwide represents a potential recurring revenue stream through accessories, replacement parts, and software subscriptions. For a buyer with manufacturing scale and an existing distribution network, reviving the brand at a more competitive price point could be viable.

The Outlook

iRobot's bankruptcy is more than a single company's failure. It is a cautionary lesson about the economics of hardware innovation in a globalized market. Building the first successful product in a new category creates demand, but it does not create a moat. The technology that made Roomba revolutionary in 2002 was replicable by 2018, and by 2024 it was available at commodity prices from manufacturers with structural cost advantages that no amount of R&D spending could overcome. The Roomba itself will almost certainly survive under new ownership. The question is whether the next generation of hardware pioneers, in robotics, wearables, or any emerging category, can find a business model that avoids the trap iRobot fell into: creating the market and then losing it.

Sources

- How iRobot Lost Its Way Home - TechCrunch, December 2025

- Former iRobot CEO Calls Roomba Maker's Bankruptcy 'A Tragedy for Consumers' - CNBC, December 2025

- Roomba Maker Files for Bankruptcy, Weighed Down by Debt and Tariffs - NPR, December 2025

- A Roomba Recorded a Woman on the Toilet. How Did Screenshots End Up on Facebook? - MIT Technology Review, December 2022

- iRobot Cofounder Colin Angle: Roomba-Maker's Biggest Reason for Failure Was Chinese Competitors - Fortune, December 2025