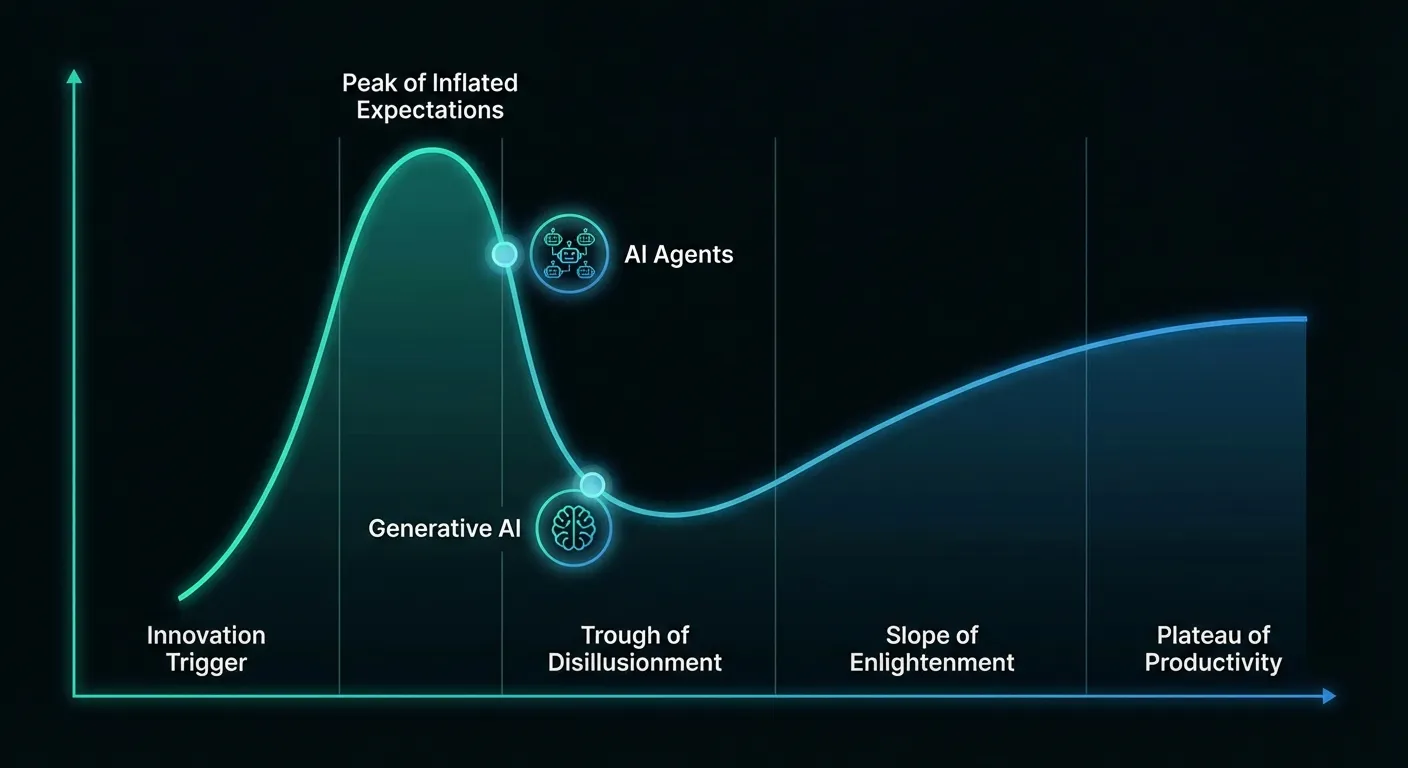

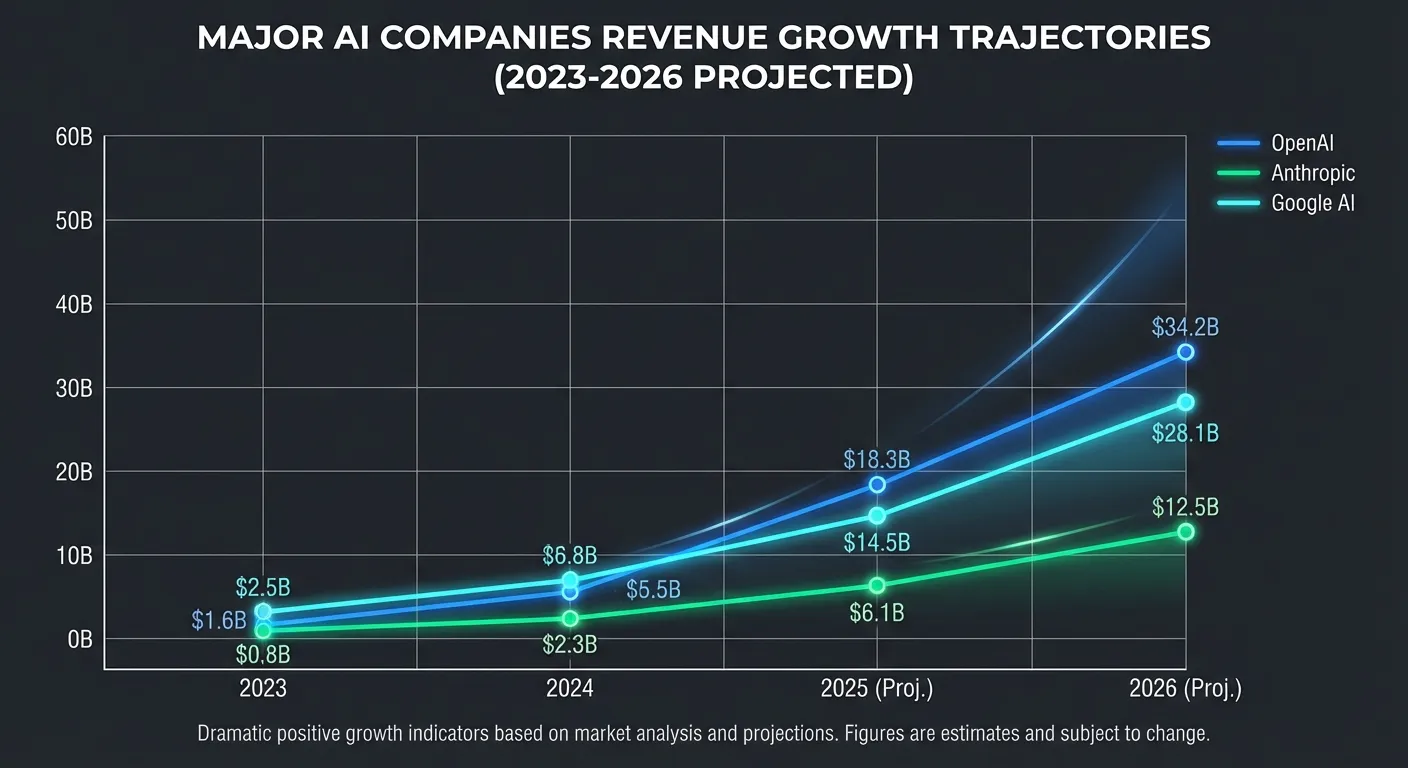

The AI industry enters 2026 with a paradox that's confusing investors, executives, and analysts alike. Gartner has placed generative AI firmly in the "trough of disillusionment," the phase of its famous hype cycle where technologies fail to meet inflated expectations and enthusiasm collapses. MIT Sloan Management Review columnists are predicting "deflation of the AI bubble and subsequent hits to the economy" as one of their top trends to watch. Yet OpenAI generated more than $13 billion in revenue during 2025 and is targeting $30 billion for 2026. Anthropic expects to triple its revenue from $4.7 billion to $15 billion. The contradiction between bubble warnings and explosive growth isn't easily resolved, but understanding it matters for anyone making decisions about AI investments, careers, or strategy.

The truth is that both narratives are partially correct, and they're describing different parts of the same elephant. AI hype has exceeded reality in many specific applications, leading to disappointment and retrenchment. Simultaneously, AI is generating genuine economic value that's showing up in revenue numbers. Whether this constitutes a bubble depends entirely on whether you're looking at valuations, expectations, or actual business results.

The Case for the Bubble

Start with valuations. Aswath Damodaran, professor of finance at NYU Stern and widely regarded as the "Dean of Valuation," has warned that the AI industry would need to generate "two, three, four trillion in revenues eventually" to justify the capital currently being poured into it. AI startups have raised money at valuations that assume world-changing adoption, and that adoption hasn't uniformly materialized. Companies valued at billions of dollars are discovering that enterprise sales cycles are long, integration is complex, and customers are cautious about becoming dependent on rapidly evolving technology. Some of these companies will grow into their valuations; others won't survive the adjustment.

The Gartner placement reflects this reality. As John Lovelock, distinguished vice president analyst at Gartner, has noted, because AI is in the Trough of Disillusionment throughout 2026, it will "most often be sold to enterprises by their incumbent software provider rather than bought as part of a new moonshot project." Generative AI tools have been deployed widely but often failed to deliver promised productivity gains. The enterprise software sector has seen particular disillusionment: companies bought AI tools expecting transformation and got incremental improvement at best. The gap between demos and production deployments remains wide. AI that performs impressively in controlled settings often struggles with the messiness of real business data and processes.

The consulting firms have noticed. AlixPartners predicts AI-driven disruption will cause M&A activity in enterprise software to surge 30 to 40 percent year over year, reaching an estimated $600 billion in 2026. This isn't optimism; it's a prediction that weaker companies will be acquired or fail. The "disruption" language is polite framing for an expectation that many current AI companies won't survive independently.

Labor market tensions add to bubble concerns. Sixty-one percent of employees expect their job role will change significantly in 2026 due to AI, and nearly half worry about obsolescence by 2030. Yet the actual displacement has been slower and more selective than feared. Companies that announced AI-driven workforce reductions have often quietly continued hiring. The gap between anticipated AI impact and actual AI impact suggests inflated expectations.

The Case Against the Bubble

Now consider the revenue numbers. OpenAI's growth from effectively zero to $13 billion in about three years is not speculation; it's measurable business activity. Someone is paying for these services, and they're paying at scale. ChatGPT has 800 million weekly active users processing over a billion prompts daily. This is real usage, not hype.

The enterprise adoption, while slower than hoped, is happening. When Andy Markus, AT&T's chief data officer, predicts that fine-tuned small language models will become standard in mature enterprises, he's describing a practical deployment pattern that companies are already pursuing. The shift from experimentation to production is genuine, even if it's taking longer than early projections suggested.

Physical AI and robotics represent entirely new economic activity. The announcements at CES 2026 about NVIDIA's partnerships with manufacturing companies describe applications that didn't exist five years ago. When factories use AI-powered digital twins to optimize production, that's not bubble economics; it's productivity improvement that shows up in output per worker.

The venture capital landscape provides another data point. While some AI investments have disappointed, the leading companies continue raising money at increasing valuations from sophisticated investors who've done extensive due diligence. Anthropic's recent funding rounds, Google's continued investment in DeepMind, and Microsoft's ongoing OpenAI partnership all suggest that knowledgeable investors see value, not just hype.

The comparison to previous bubbles also offers perspective. The dot-com bubble involved companies with no revenue and no clear path to revenue, valued at billions of dollars on speculation alone. Today's leading AI companies have substantial revenue, growing rapidly, from identifiable customers paying for identifiable services. The business model exists; the question is whether growth justifies valuation.

What's Actually Happening

The most accurate picture is probably somewhere in between the extremes. AI is simultaneously overhyped in some applications and underhyped in others. The specific failures and disappointments are real, but so is the broader capability advancement.

Consumer AI applications faced inflated expectations because language models are impressive in ways that don't always translate to practical value. Writing assistance, summarization, and question answering are useful but not transformative for most people. The gap between "this is cool" and "this changes how I work" turned out to be wider than early adopters assumed.

Enterprise AI applications faced different challenges: integration complexity, data quality issues, and organizational resistance. The technology often works in isolation but fails when connected to legacy systems with inconsistent data and complicated access controls. Enterprises are learning that AI deployment is a systems problem, not just a technology problem.

Meanwhile, specialized AI applications are advancing rapidly without much hype. Medical imaging analysis, drug discovery acceleration, and materials science research are all areas where AI provides genuine advantages. These applications don't make headlines because they're not consumer-facing, but they're creating economic value.

The China factor complicates analysis. Chinese AI models, often released as open source, have demonstrated that frontier capabilities don't require frontier budgets. DeepSeek's R1 model showed that small teams can produce competitive AI. This changes the competitive dynamics: if capability can be replicated cheaply, the sustainable advantage shifts from model training to data access, distribution, and integration.

What to Watch

For investors, the key question is whether revenue growth continues at current rates. The companies that prove their business models sustainable will separate from those that can't convert usage into profits. OpenAI's $30 billion 2026 target is ambitious; whether they hit it matters enormously for market confidence.

For enterprises considering AI adoption, the lesson from the hype cycle is to focus on specific, measurable applications rather than transformational visions. The companies finding value from AI are typically those with clear use cases, clean data, and realistic expectations. The transformation will be incremental, not revolutionary, and planning should reflect that reality.

For employees worried about displacement, the pattern so far suggests more job evolution than job elimination. Roles that involve routine cognitive tasks are at risk, but the full automation predicted by AI optimists hasn't materialized. Learning to work with AI tools seems more valuable than worrying about replacement by them.

The Outlook

The AI bubble question resolves differently depending on which segment you examine. The most vulnerable to correction are AI-powered enterprise software startups valued at over $1 billion with fewer than $100 million in annual revenue. These companies raised money on transformation narratives but face long sales cycles, integration complexity, and incumbents bundling AI features for free. Consumer AI wrappers, apps built as thin layers on top of foundation models with no proprietary data or distribution advantage, are similarly exposed. When the underlying models improve, these wrappers become redundant.

The most durable segments are the foundation model providers themselves (OpenAI, Anthropic, Google) whose revenue growth is measurable and accelerating, the semiconductor companies supplying AI infrastructure where demand remains supply-constrained, and specialized AI applications in healthcare, materials science, and industrial automation where the technology solves specific, measurable problems rather than promising vague transformation.

The next twelve months will sharpen this picture. The AI model wars currently underway will determine which companies capture lasting value and which were bidding up prices in a game of musical chairs. Watch earnings reports over the next two quarters for the gap between projections and reality. Watch enterprise deployment patterns: are companies moving from pilots to production, or quietly abandoning AI initiatives? And watch for the first major AI company to miss targets significantly. That moment will test market confidence in ways that have not been tested yet.

Sources

- What's Next for AI in 2026 - MIT Technology Review, January 2026

- Five Trends in AI and Data Science for 2026 - MIT Sloan Management Review, January 2026

- In 2026, AI Will Move from Hype to Pragmatism - TechCrunch, January 2026

- Gartner Says Worldwide AI Spending Will Total $2.5 Trillion in 2026 - Gartner, January 2026

- Enterprise Technology 2026: 15 AI, SaaS, Data Business Trends to Watch - Constellation Research, January 2026