The first major economic report of 2026 arrived Friday morning with a thud. The Bureau of Labor Statistics reported that employers added just 50,000 jobs in December, significantly below the 73,000 that economists had forecast. The unemployment rate ticked up to 4.4 percent, its highest level since late 2024. For a Federal Reserve that spent 2025 carefully calibrating interest rate cuts, the report raises uncomfortable questions about whether the central bank acted too aggressively, not aggressively enough, or whether factors beyond monetary policy are now driving the labor market.

The headline number tells only part of the story. Underneath the disappointing topline are sector-specific trends that reveal an economy in transition. Healthcare and food services continue adding workers, while retail shed jobs during what should have been a hiring season. The report arrives in the shadow of last year’s 43-day government shutdown, which disrupted BLS data collection and may have affected the quality of December’s figures. Still, the pattern of weakening job growth has been evident for months, and Friday’s report confirms rather than contradicts that trajectory.

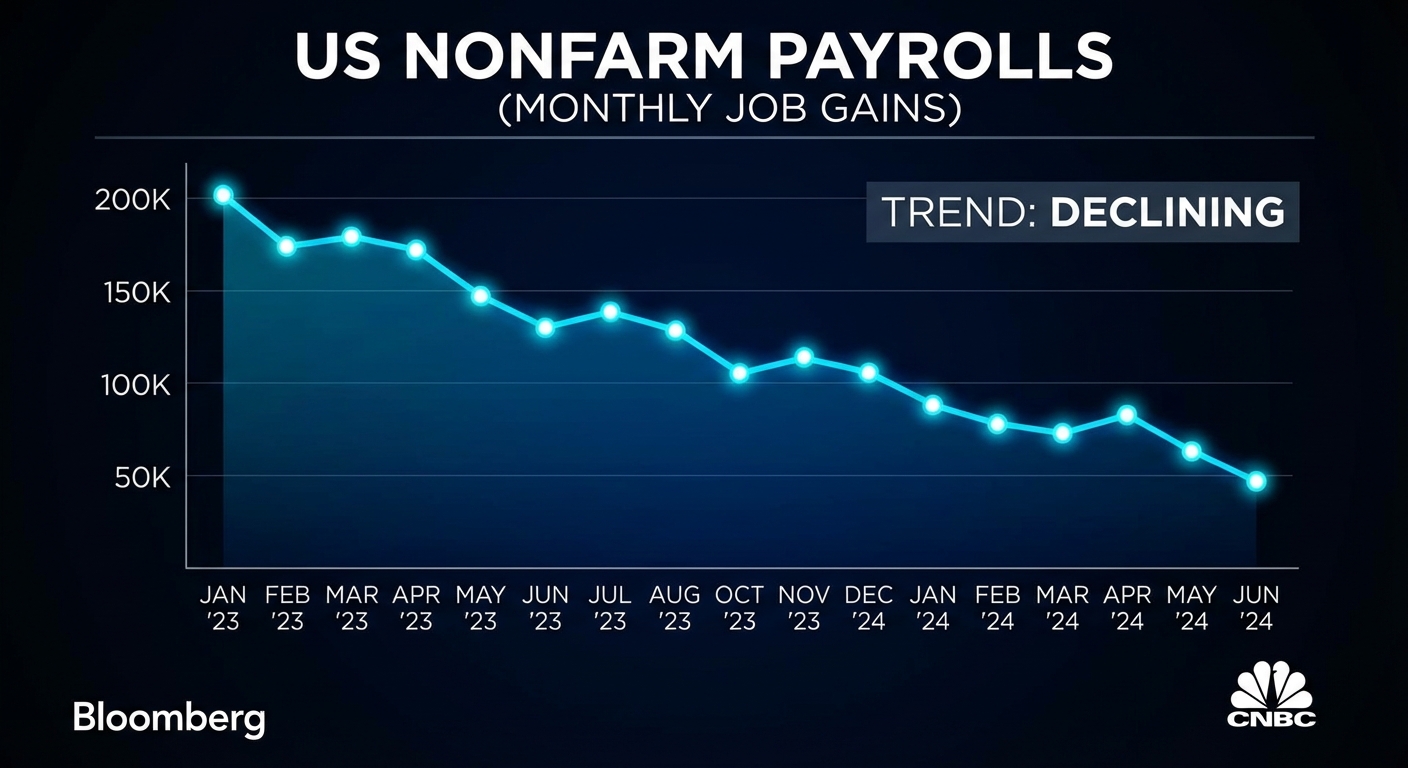

What the Numbers Show

The December employment report covers the final month of 2025 and represents the economy’s state as the new year begins. The 50,000 jobs added represent a significant slowdown from the 150,000 to 200,000 monthly gains that characterized much of 2024. The unemployment rate rising to 4.4 percent, while still low by historical standards, continues an upward drift that began last summer.

Sector performance varied considerably. Food services and drinking places added 27,000 positions, continuing a trend driven by consumer spending on dining and entertainment. Healthcare added 21,000 jobs, reflecting both demographic demand from an aging population and the sector’s relative insulation from economic cycles. Social assistance added 17,000 positions, another healthcare-adjacent category that tends to grow steadily regardless of broader conditions.

Retail trade lost 25,000 jobs, a concerning signal given that December typically sees holiday hiring. The losses suggest that retailers either hired less than usual for the holiday season, laid off seasonal workers earlier than in past years, or both. Combined with anecdotal reports of weak holiday sales at traditional retailers, the retail job losses point to structural changes in consumer behavior that COVID accelerated and that show no signs of reversing.

The report also contains important technical caveats. Data collection was disrupted by the government shutdown that ended in December. Response rates from surveyed establishments may have been lower than usual, introducing uncertainty into the estimates. The BLS flagged that its February report will include annual benchmark revisions that could significantly alter our understanding of the labor market’s trajectory throughout 2024 and into 2025.

The Federal Reserve’s Dilemma

The Federal Reserve cut interest rates several times during 2025, responding to slowing inflation and signs of labor market cooling. Friday’s report will factor into the central bank’s next meeting later this month, though it’s unlikely to trigger immediate policy changes. Fed officials have emphasized that they make decisions based on the totality of data rather than any single report, and January brings additional information including inflation figures and another employment report before the next rate decision.

The debate within the Fed has centered on whether the economy is achieving a “soft landing,” meaning a return to normal from pandemic distortions without triggering a recession, or whether more aggressive action is needed to support growth. Hawks within the institution have worried that rate cuts risked reigniting inflation just as it approached the 2 percent target. Doves have argued that restrictive policy kept in place too long risks unnecessary economic damage and job losses.

Friday’s report provides ammunition for both camps. The weaker-than-expected job growth suggests the economy may need more support, validating those who pushed for rate cuts. But the continued, if slower, job growth also indicates the economy isn’t falling off a cliff, supporting those who counseled patience. Fed Chair’s post-meeting press conference will likely emphasize the bank’s data-dependent approach while offering few concrete commitments about the rate path ahead.

Market reactions to Friday’s report were relatively muted, suggesting investors had already priced in some degree of labor market softening. Treasury yields moved slightly higher as traders recalibrated expectations for future Fed actions. Stock futures showed modest losses that could reverse as the trading day progresses. The lack of dramatic market movement indicates that Friday’s numbers, while below consensus, didn’t fundamentally surprise investors who have been watching the same trends economists have.

What’s Driving the Slowdown

The labor market’s cooling reflects multiple forces, some transitory and some structural. The end of pandemic-era stimulus and excess savings has normalized consumer demand after years of unusual strength. Higher interest rates, even as they’ve begun declining, have slowed housing construction and related industries. Technology sector layoffs that began in 2024 have continued, though at a slower pace, as companies that overhired during the boom adjust their workforces.

The retail losses point to a particularly important structural shift. Consumers increasingly shop online, reducing the need for in-store workers. Those who do visit physical stores expect fewer employees and more self-service options. The seasonal hiring surge that once characterized December at major retailers has diminished as companies build leaner year-round operations supplemented by temporary workers during peak periods. These trends existed before the pandemic but accelerated dramatically during it and show no signs of reversing.

Immigration policy may also be affecting labor supply in ways the data doesn’t fully capture. The Trump administration’s expanded enforcement operations have reportedly made some workers reluctant to seek employment, while reduced legal immigration limits the flow of workers into sectors that have traditionally relied on immigrant labor. Agriculture, construction, and food processing have all reported labor shortages that the domestic workforce hasn’t filled. Whether these shortages eventually drive up wages or simply constrain economic activity remains to be seen.

The government shutdown created an unusual confounding factor for December’s data. Federal workers were furloughed, federal contractors saw operations disrupted, and businesses throughout the Washington D.C. region and beyond felt ripple effects. The BLS attempted to adjust for these factors, but measurement error likely increased. The February report will include revisions that may significantly change our understanding of what actually happened in the labor market during late 2025.

What to Watch

The immediate question is whether December’s weakness represents a one-time disappointment or the beginning of a more sustained downturn. January’s employment report, released in early February, will provide the next major data point. If job growth remains weak, pressure will build on the Fed to cut rates more aggressively. If December proves to be an outlier and growth rebounds, the soft landing narrative regains credibility.

Watch for the benchmark revisions in February, which could revise 2024’s job growth significantly higher or lower. Past revisions have sometimes changed the story substantially. A downward revision would suggest the labor market was weaker throughout the year than we thought, while an upward revision would make December’s weakness look more like normalization after unusually strong performance.

The inflation picture remains central to Fed decision-making. Even with weaker job growth, if inflation proves stubborn, the central bank will be reluctant to cut rates aggressively. The upcoming Consumer Price Index report will receive intense scrutiny alongside employment data. The Fed’s challenge is balancing its dual mandate of maximum employment and price stability when those goals may require different policy responses.

The Bottom Line

December’s jobs report shows an economy that has clearly cooled from the unsustainable pace of recent years but isn’t collapsing. The 50,000 jobs added, while below expectations, still represents growth. The 4.4 percent unemployment rate, while rising, remains below historical averages. The question isn’t whether the economy is strong or weak but whether it’s stabilizing at a sustainable level or continuing to deteriorate.

For workers, the practical implications are a job market that has clearly shifted from the worker-friendly conditions of 2022 and 2023 to something more normal. Fewer job openings, less aggressive salary offers for job hoppers, and more caution from employers about headcount growth characterize the current environment. For businesses, the report suggests consumer demand may continue softening, warranting caution about expansion plans. For investors, Friday’s data adds one more piece to a puzzle that remains fundamentally uncertain about the economy’s direction.

Sources: Bureau of Labor Statistics, CNBC, Bloomberg, MarketPulse, Yahoo Finance.